Table of Contents

- Why Bookkeeping Mistakes Are More Dangerous Than Most Business Owners Realize

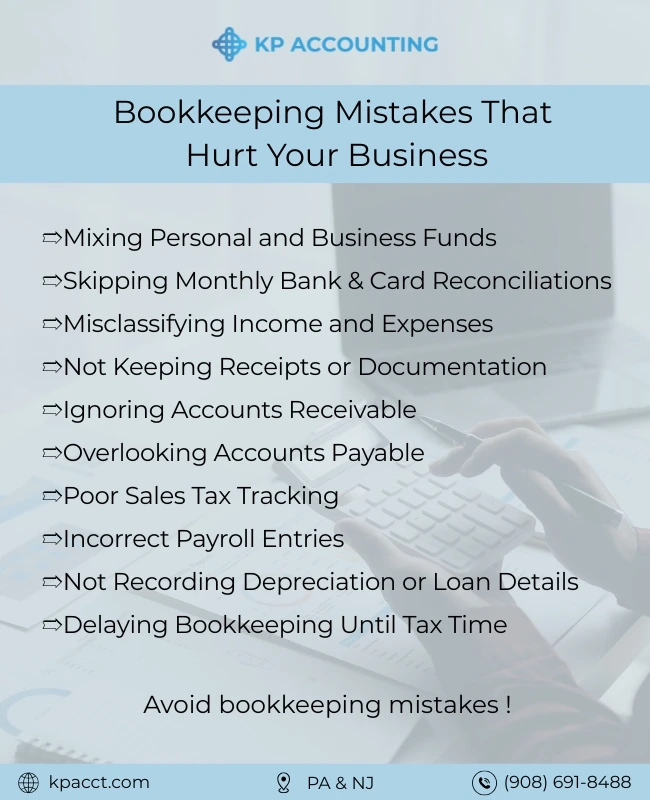

- The 10 Most Common Bookkeeping Mistakes (and How to Avoid Them)

- How Bookkeeping Errors Affect Your Business

- How to Avoid Bookkeeping Mistakes

- Q&A

- CONCLUSION – Bookkeeping Mistakes Are Preventable When You Have the Right System

Yet despite its importance, bookkeeping errors remain one of the most widespread and costly issues among U.S. small businesses. Some errors are minor and easy to correct. Others can trigger IRS penalties, inflated tax bills, inaccurate financial reporting, or even long-term cash-flow damage.

This comprehensive, CPA-style guide breaks down the 10 most common bookkeeping mistakes, why they occur, what consequences they create, and most importantly how to avoid bookkeeping mistakes before they impact your business.

Why Bookkeeping Mistakes Are More Dangerous Than Most Business Owners Realize

Many entrepreneurs assume bookkeeping mistakes are harmless or easily fixable. But in reality, bookkeeping errors compound over time, often becoming more difficult and more expensive to correct.

Here’s why bookkeeping mistakes are so damaging:

1. Minor errors grow into structural problems.

One miscategorized transaction may not hurt you, but hundreds will distort your financial statements.

2. IRS penalties accumulate quickly.

Inaccurate tax filings, missing documents, and improperly recorded deductions are among the top causes of audits.

3. Bookkeeping errors distort business decisions.

You can’t make informed decisions with incorrect numbers.

4. Cash-flow problems multiply.

Unreconciled accounts or untracked expenses can create cash shortages at the worst possible moments.

5. Fixing errors later is far more expensive.

Accountants spend significantly more hours cleaning bad books than maintaining clean ones.

6. Poor bookkeeping lowers your business valuation.

Lenders, investors, and buyers depend heavily on accurate books.

The 10 Most Common Bookkeeping Mistakes (and How to Avoid Them)

Below is a detailed breakdown of the most frequent bookkeeping mistakes U.S. small businesses make, supported by professional CPA insights.

1. Mixing Personal and Business Finances

This is the #1 bookkeeping mistake across the United States and one of the most damaging.

How this mistake happens:

- Owners use personal cards for business purchases

- Owners pay personal expenses from business accounts

- Transfers are not documented properly

- Reimbursements are not tracked

Consequences:

- Distorted financial reports

- Incorrect tax deductions

- High IRS audit risk

- Difficulty identifying actual profits

- Compromised liability protection for LLCs

How to avoid this mistake:

- Maintain separate bank accounts

- Use dedicated business credit cards

- Use reimbursement forms for personal-to-business expenses

- Never co-mingle funds

- Use accounting software to track owner’s draws and contributions

2. Failing to Reconcile Bank and Credit Card Accounts Monthly

Bank reconciliation ensures that your accounting records match your bank statements.

Skipping this step creates accounting discrepancies that grow quickly.

Common causes:

- Relying on automatic bank feeds

- Ignoring small unmatched transactions

- Not reviewing statements line by line

Consequences:

- Missing deposits

- Duplicate expenses

- Incorrect cash balance

- Hidden fraudulent transactions

- Inaccurate profit and loss (P&L) reports

How to avoid this mistake:

- Reconcile every account every month

- Verify deposits, withdrawals, and transfers

- Flag any unexpected charges immediately

- Ensure software connections are working properly

Even a single unreconciled month can cause long-term reporting issues.

3. Misclassifying Income and Expenses

Incorrect categorization is among the most damaging bookkeeping errors.

Why it happens:

- Business owners categorize based on assumptions

- Software rules are not correctly configured

- Generic categories like “Miscellaneous” are overused

- Revenue streams blend together

Consequences:

- Overstated or understated tax deductions

- Incorrect profit margins

- Misleading financial statements

- Difficulty preparing for tax season

- Audit triggers due to unusual categorization patterns

How to avoid this mistake:

- Use IRS-approved business categories

- Ask your CPA to create a customized chart of accounts

- Avoid using “Miscellaneous”

- Update categorization rules periodically

Accurate categorization leads to more accurate tax planning and better business intelligence.

4. Not Keeping Proper Receipts and Documentation

Receipts are the foundation of bookkeeping accuracy.

Without documentation, your expenses may be disallowed during IRS reviews.

Why receipts get lost:

- Business owners forget to collect them

- Paper receipts fade or get damaged

- Digital receipts stay in inboxes without organization

- No document storage system exists

Consequences:

- Lost tax deductions

- IRS disallowances

- Inaccurate expense tracking

- Difficulty proving business purpose

How to avoid this mistake:

- Use a receipt-scanning app (QuickBooks, Dext, Shoeboxed)

- Save e-receipts to a cloud folder

- Organize receipts by month

- Attach receipts directly to transactions in your accounting software

Documentation protects you from financial and legal consequences.

5. Ignoring Accounts Receivable (Unpaid Invoices)

Many small businesses are profitable on paper but suffer cash-flow shortages because clients don’t pay on time.

Why receivables get ignored:

- No system for tracking overdue invoices

- No automated reminders

- Avoidance of uncomfortable follow-up conversations

- Manual invoicing processes

Consequences:

- Cash shortages

- Incorrect revenue reporting

- Difficulty funding payroll or expenses

- Higher likelihood of bad debt

How to avoid this mistake:

- Implement automated invoicing

- Set clear payment terms (NET 15 or NET 30)

- Send reminders one week before due dates

- Charge late fees

- Track A/R weekly

Unpaid invoices destroy cash flow monitoring them is non-negotiable.

6. Overlooking Accounts Payable (Unpaid Bills)

Just as customers owe you money, you owe vendors money and ignoring this can harm your business relationships.

Why this mistake occurs:

- Bills come through email and are forgotten

- No systematic approval workflow

- Business owners confuse unpaid bills with expenses

Consequences:

- Late fees

- Damaged vendor relationships

- Service interruptions

- Difficulty negotiating payment terms

- Cash-flow mismanagement

How to avoid this mistake:

- Use accounting software to enter bills upon receipt

- Review payables weekly

- Set automated reminders

- Plan cash flow around due dates

A well-managed A/P system improves credibility and financial stability.

7. Not Tracking Sales Tax Properly

Sales tax regulations vary by state and errors are common among U.S. small businesses.

Common issues:

- Not recording sales tax separately

- Commingling sales tax with revenue

- Not reconciling collected tax vs. tax owed

- Failing to register in required states

Consequences:

- Overpayment or underpayment of sales tax

- State-level penalties

- Tax notices and audits

- Cash-flow shortages due to unexpected tax bills

How to avoid this mistake:

- Track sales tax as a liability, not income

- Use POS systems that calculate tax automatically

- Reconcile sales tax monthly

- Hire a CPA for multi-state tax compliance

Sales tax mistakes are among the most costly bookkeeping errors.

8. Incorrect Payroll Recording

Payroll is one of the most regulated areas of accounting, and mistakes here can lead to serious compliance issues.

Why payroll errors happen:

- Misclassified employees (W-2 vs 1099)

- Incorrect tax withholding

- Late payroll tax payments

- Unrecorded reimbursable expenses

- Failure to track PTO or overtime

Consequences:

- IRS and state penalties

- Incorrect labor cost reporting

- Employee dissatisfaction

- Payroll tax liabilities

How to avoid this mistake:

- Use reliable payroll software

- Review payroll reports monthly

- Ensure each employee’s classification is correct

- Record payroll expenses and liabilities accurately

Payroll should rarely be manual, automation prevents costly mistakes.

9. Ignoring Depreciation, Loans, and Interest Tracking

Many small business owners forget to record depreciation or loan details.

Why this mistake happens:

- Lack of understanding of loan amortization

- Depreciation schedules seem complicated

- Owners focus only on cash transactions

Consequences:

- Incorrect asset values

- Overstated profits

- Missed tax deductions

- Financial statements that misrepresent business health

How to avoid this mistake:

- Record loan principal and interest separately

- Maintain depreciation schedules for fixed assets

- Collaborate with your CPA quarterly

- Use accounting software that automates depreciation

Ignoring these adjustments leads to misleading financial reports.

10. Delaying Bookkeeping Until Tax Season

The biggest bookkeeping mistake: waiting until the end of the year.

Why this happens:

- Bookkeeping feels time-consuming

- Business owners get busy

- “I’ll do it later” becomes a habit

Consequences:

- Overwhelming backlog

- Higher accounting costs

- Lost deductions

- Stress, errors, and inaccurate filings

- Risk of missed tax deadlines

How to avoid this mistake:

- Maintain a monthly bookkeeping checklist

- Set aside 1 hour per week

- Automate income and expense categorization

- Outsource if you fall behind

Timely bookkeeping is the difference between clarity and chaos.

How Bookkeeping Errors Affect Your Business

Bookkeeping errors have direct and indirect consequences that accumulate over time.

Financial Consequences

- Overpaying taxes

- Unexpected tax bills

- Cash-flow shortages

- Missed revenue due to untracked A/R

- Unnecessary business expenses

Legal & Compliance Consequences

- IRS penalties

- State tax notices

- Payroll compliance violations

- Higher audit risk

Operational Consequences

- Wrong pricing decisions

- Misleading profit margins

- Poor budgeting

- Difficulty securing loans

- Inability to forecast revenue

Strategic Consequences

- Investors and lenders lose confidence

- Business valuation decreases

- Expansion becomes risky

- Owners make decisions based on inaccurate numbers

Accurate bookkeeping is not optional, it is essential for long-term stability.

How to Avoid Bookkeeping Mistakes

1. Use Cloud-Based Accounting Software

QuickBooks, Xero, or Zoho Books significantly reduce manual errors.

2. Automate As Much As Possible

- Bank rules

- Recurring invoices

- Payroll

- Expense categorization

3. Maintain a Regular Bookkeeping Schedule

Weekly or monthly consistency prevents backlog.

4. Hire a Qualified Bookkeeper or CPA

Especially when your financial activity increases.

5. Keep Tax Planning and Bookkeeping Connected

Tax mistakes often start from bookkeeping mistakes.

6. Conduct Monthly Reviews

P&L, Balance Sheet, Cash Flow, A/R, A/P.

7. Separate Personal and Business Expenses

Never merge your finances in any circumstance.

8. Use a Receipt Management System

Store digital copies to avoid IRS problems.

9. Reconcile All Accounts Monthly

This ensures data accuracy.

10. Conduct a Year-End Financial Clean-Up

Before tax season begins.

Q&A

What are the most common bookkeeping mistakes?

What are the consequences of bookkeeping errors?

How can small businesses avoid bookkeeping mistakes?

Why is accurate bookkeeping important for small businesses?

CONCLUSION – Bookkeeping Mistakes Are Preventable When You Have the Right System

Bookkeeping mistakes are common but they are entirely preventable with the right tools, routines, and professional support. By understanding the ten most damaging bookkeeping errors and implementing the preventive steps outlined here, your business can avoid financial inaccuracies, reduce tax liabilities, strengthen cash flow, and maintain complete compliance with U.S. accounting standards.